put call parity binary options

What is Put-Call Parity?

Put-call parity is an important concept in options pricing which shows how the prices of puts , calls , and the underlying asset must be consequent with one some other. This equation establishes a relationship between the price of a phone call and put choice which have the same underlying asset. For this human relationship to work, the phone call and put option must have an identical expiration appointment and strike price.

The put-phone call parity human relationship shows that a portfolio consisting of a long call selection and a short put option should be equal to a forward contract with the same underlying asset, expiration, and strike price. This equation can be rearranged to show several culling ways of viewing this relationship.

Summary

- Put-call parity is an of import relationship between the prices of puts, calls, and the underlying asset

- This relationship is only true for European options with identical strike prices, maturity dates, and underlying assets (European options can only be exercised at expiration, unlike American options that can be exercised on any date up to the expiration date)

- This theory holds that simultaneously holding a short put and long phone call (identical strike prices and expiration) should provide the same return as one forward contract with the same expiration date every bit the options and where the frontwards price is the same as the options' strike price

- Put-call parity tin can be used to identify arbitrage opportunities in the market

Put-Call Parity Excel Calculator

Below, we will become through an example question involving the put-call parity relationship. This tin can hands be washed with Excel. To download the put-call parity calculator, check out CFI's free resource: Put-Call Parity Calculator

Interpreting the Put-Call Parity

To better understand the put-call parity theory, let us consider a hypothetical state of affairs where you buy a call selection for $10 with a strike price of $100 and maturity date of one twelvemonth, every bit well every bit sell a put option for $x with an identical strike price and expiration. According to the put-call parity, that would be equivalent to buying the underlying asset and borrowing an amount equal to the strike price discounted to today. The spot price of the asset is $100 and we make the supposition that at the end of the twelvemonth the price is $110 – so, does the put-call parity hold?

If the price goes upwardly to $110, you would exercise the call option. You paid $10 for information technology but you can purchase the nugget at the strike price of $100 and sell information technology for $110, and so you net $0. You lot have too sold the put pick. Since the nugget has increased in marketplace value, the put option will not be exercised by the buyer and you pocket the $10. That leaves you with $10 from this portfolio.

What is the portfolio consisting of the underlying asset and curt position on the strike price worth at the expiration engagement? Well, if yous had invested in the asset at the spot cost of $100 and information technology ended at $110, and you had to pay back the strike toll at maturity from the corporeality you borrowed which would be $100, the net amount would be $10. Nosotros see that these two portfolios both internet to positive $10 and the put-call parity holds.

Why is the Put-Call Parity Important?

The put-call parity theory is of import to understand because this relationship must hold in theory. With European put and calls, if this human relationship does non concord, then that leaves an opportunity for arbitrage . Rearranging this formula, we can solve for whatever of the components of the equation. This allows us to create a synthetic telephone call or put option. If a portfolio of the synthetic selection costs less than the actual pick, based on put-call parity, a trader could use an arbitrage strategy to profit.

What is the Put-Call Parity Equation?

As mentioned in a higher place, the put-telephone call parity equation can exist written a number of different means and rearranged to make varying inferences. A couple of common means it is expressed are as follows:

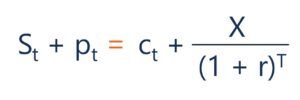

St + pt = ct + X/(1 + r)^T

The in a higher place equation shown in this combination tin can be interpreted as a portfolio property a long position in the underlying asset and a put choice should equal a portfolio holding a long position in the call selection and the strike price. Co-ordinate to the put-call parity this relationship should concord or else an opportunity for arbitrage would exist.

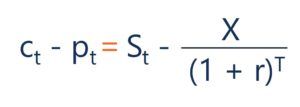

ct – pt = St – X/(1 + r)^T

In this version of the put-phone call parity, a portfolio that holds a long position in the phone call, and a short position in the put should equal a portfolio consisting of a long position in the underlying asset and a short position of the strike price.

For the above equations, the variables tin be interpreted as:

- St = Spot Price of the Underlying Asset

- pt = Put Option Price

- ct = Call Option Price

- Ten/(one + r)^T = Nowadays Value of the Strike Toll, discounted from the date of expiration

- r = The Discount Charge per unit, often the Adventure-Costless Rate

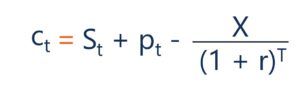

The equation can too be rearranged and solved for a specific component. For example, based on the put-telephone call parity, a constructed call selection can be created. The following shows a synthetic call selection:

ct = St + pt – Ten/(i + r)^T

Here nosotros can see that the call option should be equal to a portfolio with a long position on the underlying asset, a long position on the put option and a short position on the strike price. This portfolio can exist thought of as a synthetic call option. If this human relationship doesn't hold, then an arbitrage opportunity exists. If the synthetic phone call was less than the call option, so you could purchase the synthetic telephone call and sell the actual call option to profit.

Put-Call Parity – European Call Option Example

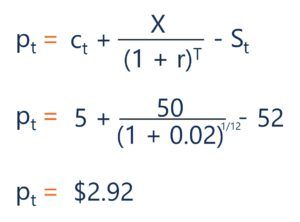

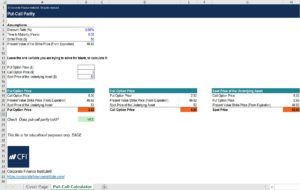

Let us now consider a question involving the put-phone call parity. Suppose a European phone call option on a barrel of crude oil with a strike toll of $50 and a maturity of 1-calendar month, trades for $v. What is the toll of the put premium with identical strike price and fourth dimension until expiration, if the i-month risk-gratis rate is ii% and the spot price of the underlying asset is $52?

Here nosotros can encounter the calculation that would be used to discover the put premium:

These calculations can also be done in Excel. The following shows the solution to the in a higher place question done in excel:

If you would like to acquire more about financial modeling, check out CFI'southward Financial Modeling Courses

Additional Resources

Thanks for reading CFI'south guide on Put-Telephone call Parity. To go on advancing your career, the additional CFI resources below will exist useful:

- Options: Calls and Puts

- Choice Pricing Models

- Arbitrage

- Derivatives

Source: https://corporatefinanceinstitute.com/resources/knowledge/finance/put-call-parity/

Posted by: newberryviser1964.blogspot.com

0 Response to "put call parity binary options"

Post a Comment